Blockchain technology has the unique potential to disrupt and improve upon countless transactions we conduct daily. Though, most information about this new tech is either too vague or too technical. So, what is blockchain technology? With this step-by-step guide for beginners, we break down this secure, transparent, and permanent system which is so much more than just a platform on which you can trade Bitcoin (BTC).

What Is Blockchain?

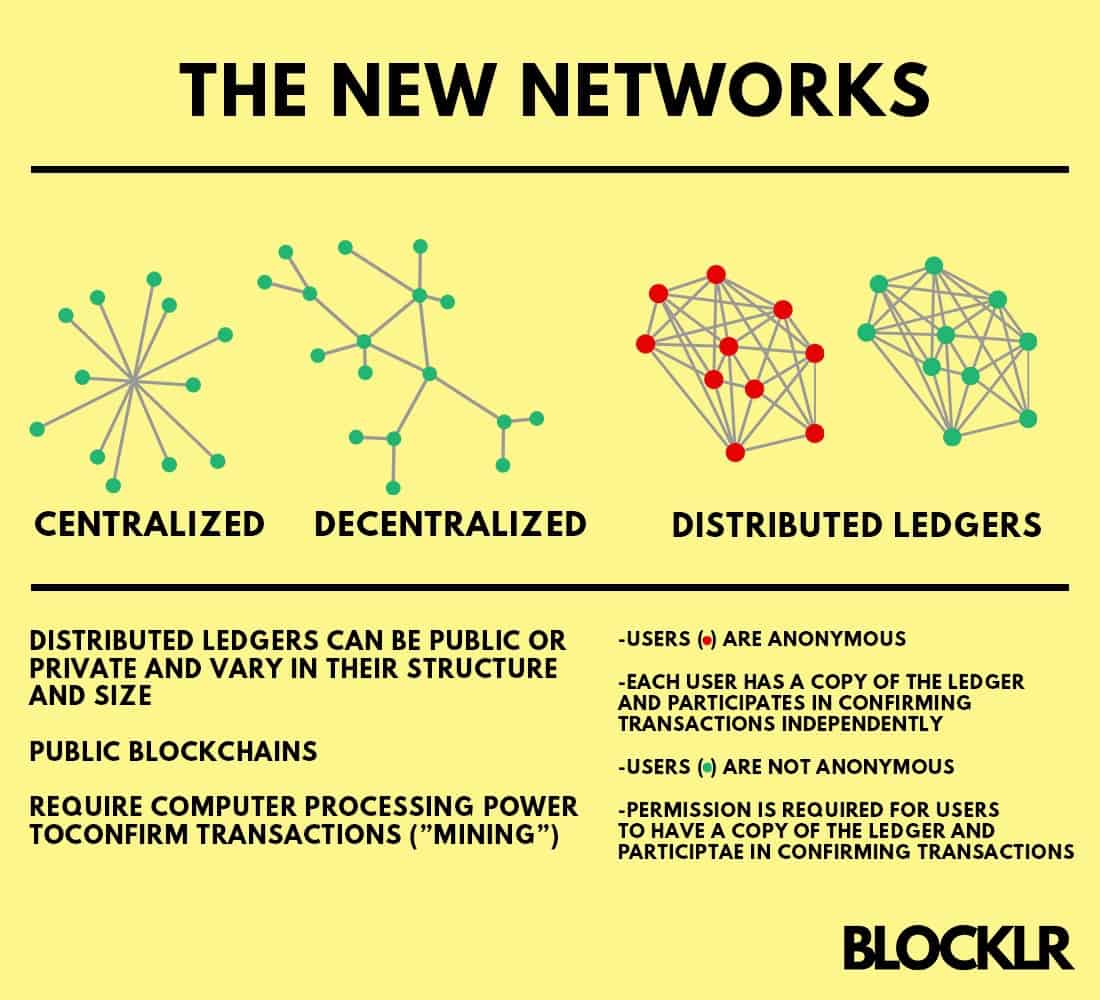

Blockchain is a system of decentralized digital lists, or ledgers, containing records referred to as “blocks.” Blocks hold information in a secure, transparent, and permanent way that everyone can access. It originally came about to record transactions done using the first cryptocurrency, Bitcoin.

What is Bitcoin? Though Bitcoin (BTC), the first cryptocurrency invented by Satoshi Nakamoto, is where blockchain began, the distributed ledger has capabilities far beyond that. Because the system is decentralized, meaning there is no central force controlling, moderating, or managing its information, there is no central database that can be corrupted or hacked.

Decentralization allows for complete transparency in all shared information. Furthermore, the network hosting of the information is impossible to tamper with. Rather than passing information back and forth, swapping ownership each time, everyone essentially owns it, and can access it, simultaneously.

This eliminates the possibility for human error. And because the verification process is so strict, the information within it is trustworthy. It cannot be altered because doing so would make the whole chain invalid. In other words, blockchain information cannot be muted or censored, and holds the possibility for autonomy and bringing responsibility and control back to the individual. More specifically, here’s how this works.

Getting to Know Blockchain Technology

There are plenty of things that we use without fully understanding. Though it is entirely possible to benefit from the blockchain technology without realizing it, it doesn’t have to be that way. Because blockchain applications incredibly vast and powerful, the technology can seem quite mysterious and confusing. The thing is, the underlying technology is actually quite simple.

There are plenty of things that we use without fully understanding. Though it is entirely possible to benefit from the blockchain technology without realizing it, it doesn’t have to be that way. Because blockchain applications incredibly vast and powerful, the technology can seem quite mysterious and confusing. The thing is, the underlying technology is actually quite simple.

A Chain of Blocks

Blockchain is a series of transactions referred to as “blocks.” Each block contains all of the information and data about one transaction, a hash. It also contains the previous block’s hash. A hash is a code that acts as the fingerprint of the block, it is completely unique to that block and changes each time the data of the transaction is altered.

Because each block contains the hash from the previous block, they can build on top of each other, forming a chain. If someone changes one block’s data, this will make the following blocks invalid since the hashes will no longer match. In which case, the change will need to go through a validation process.

This system is what makes tampering with blockchain information almost impossible. Blockchain is merely a string of chronological transactions, each referring to the last and owning a piece of the previous. If someone or thing wishes to conduct a transaction, they don’t personally edit a block or chain, they submit a request to the peer-to-peer network to be checked, validated, and approved.

Peer-to-Peer (P2P) Structure

More specifically, a P2P network moderates blockchain information. This model distributes authority and responsibility among countless nodes to eliminate bias and error.

The network is built on computers nodes that validate and relay the transactions to the blockchain. Every node acts as a blockchain network administrator and has opted to do so voluntarily. It is like a community watch that protects and manages blockchain information. The transactional data contained within it is verified by millions of computers through a process we call “mining.”

If a new transaction is made or a block is added, all nodes in a network must come to a consensus before it is validated. The Peer-to-Peer structure of the blockchain creates across-the-board accountability as both everyone and no one controls it. Blockchain information necessitates collaboration, meaning that it has no hierarchy.

Imagine blockchain technology as a democratic approach to validating, managing, and circulating the abundance of information we produce daily.

Consensus Mechanisms

Consensus mechanisms allow a P2P network to work harmoniously without anyone having to trust or even know one other. It operates on a consensus mechanism which has a set of rules to moderate the adding of blocks, assess the validity of blocks, and form conclusions about what is and is not true based on an algorithm.

The collective accountability of the consensus mechanism is what makes blockchain information trustworthy and virtually unalterable. Only in the case of a 51% attack on blockchain could an attacker modify transaction information. As these networks continue to grow, this amount of ownership is increasingly unlikely.

Proof of Work (PoW)

One of the blockchain’s consensus mechanisms is Proof of Work (PoW). The primary goal of the Proof of Work is to make it harder to create invalid blocks. The PoW is hard to produce, but simple to verify. This type of equation makes it easy to check whether the information is valid. To create a new block, miners complete a PoW which includes all of that block’s data. The first miner to solve the problem receives a reward.

In essence, PoW controls the speed at which miners can create blocks. For example, miners can only create a Bitcoin block every 10 minutes. This controlled speed also protects the blockchain from hackers. It ensures that each transaction connects to the previous one and the next.

Proof of Stake (PoS)

Proof of Stake is another means to validate transactions and come to a consensus. PoS and PoW have the same objective but function differently.

By comparison, PoS awards the creation of the new block depending on wealth, meaning stake. Miners in a PoS system are “forgers.” Rather than winning a block reward, forgers receive transaction fees once they’ve completed their task. Different blockchains and functions implement different consensus mechanisms.

Smart Contracts

To put it simply: a smart contract is a digital contract. But unlike your average contract, smart contracts exist on a blockchain and have a preset list of terms and conditions that regulate a specific transaction. These conditions are immutable, meaning you cannot change or violate once you agree to them. They’re also distributed, meaning all involved parties share access and control.

Since all parties can see the smart contract, all parties know when someone attempts an invalid action. And the collective won’t validate that action, so it never appears on the blockchain. Smart contracts can automate bank deposits, insurance claims, employment contracts, legal contracts, copyrights, mortgage loans, and more.

Many smart contracts are already in place. For example, a broker or a lawyer wouldn’t need to be involved in verifying agreements. In other words, a digital record sometimes already has a digital signature.

Blockchain technology by no means ends there, but to understand the blockchain fully, you must first understand how it applies to you and your life.

Real World Blockchain Applications

A common misunderstanding is that blockchain is just one system for verifying transactions or holding, trading or spending cryptocurrency.

However, blockchain is a jumping off point. This technology foundation opens up the possibilities to build new social and economic models in our world. People, companies and organizations, bots, computers, and algorithms will be able to exchange information and transact in real time—independently of politics and conflict.

How to Use Blockchain

Take a moment and think about your life. Consider what types of transactions you make each day, week, month, and year. Think about how you currently store your data. Your medical records, financial information, legal documents, and even personal identity information.

Take note of your answers to the above questions and answer this final question: who owns and controls this information? Blockchain offers the possibility to take the ownership out of the hands of centralized organizations and place it back in the hands of the actual owner.

How will you be impacted by blockchain, and what can blockchain do for you? These are many applications of blockchain technology that can benefit everyday life. Here are a few examples.

Basic Transactions

Basic transactions using cryptocurrency can be done on the blockchain by submitting a request and waiting for it to be validated. If you are looking to exchange goods or services that would benefit from having a long lasting ledger, the blockchain is an excellent means to do so safely and securely.

Banking

With centralized banking systems, the consumer is dependent on the bank to complete and record any and all transactions that you would want or need to conduct at all times. Additionally, there is a dependency on the teller to provide correct information, the ATM to function correctly, the online banking app to run smoothly; the list goes on.

Blockchain information means that you no longer have to trust third parties. It eliminates the middleman. First shifting authority to the collective eventually brings the power and responsibility back to the individual. Coins, like Akoin, are popping up to level the banking playfield in countries with less access to banking.

Ethical Consumerism

When looking to shop mindfully and ethically, blockchain technology can track goods right to the source by following a chain of information. Imagine what record keeping of this sort could do to transform corrupt or exploitative industries.

It also forces suppliers and employers to be transparent about how they create their goods. This would ensure fairer compensation for manufacturers, too. Which has the potential to end the exploitation of workers making less than a minimum wage, or in unfair and unjust working situations. For example, a new blockchain tool for appraising diamonds seeks to end blood diamonds and make purchasing ethical again.

Blockchain Crowdfunding or ICOs

Crowdfunding is a tool to help innovators and creatives in generating funding for various projects. Countless crowdfunding platforms exist, but they’re, for the most part, centralized bodies that charge fees and influence their projects. The problem with this type of crowdfunding is that the campaign owner and the investors must trust that this third company will handle their money in accordance with their agreement.

Blockchain crowdfunding decentralized this type of collective funding model. This allows individuals and organizations to maintain control and collect the entirety of the funds raised. In blockchain crowdfunding, startups create a digital currency that early investors can purchase. This is what we call an Initial Coin Offering or ICO.

Blockchain Sharing

Sharing platforms like Uber and Airbnb are increasingly popular. And today, these centralized companies keep most of the money the sharing economy generates.

With the use of blockchain sharing, the buyer can directly transfer funds to the services provider. This all occurs without an intermediary taking a portion of the money. This way, two-party transactions are entirely transparent and entirely trackable.

Tracking Distribution

Shipping, especially internationally, is costly and complicated. According to IBM, putting information on a distributed ledger will save 1/5 on transportation costs. For that reason, IBM teamed up with shipping giant Maersk to create a shipping platform.

Not only that, but it can store shipment information, thereby letting authorities known that the entire supply chain is following the law.

Stock Trading

Blockchain technology can increase security, tracing, trust, and transparency within the stock market. With shared and accessible information, blockchain information allows individuals to gather stock market information. Additionally, third-party representative won’t buy and sell stock. Instead, one individual or business will sell it to the next.

Governance

Imagine a world in which the public moderated voting and everyone could see the results immediately. Polls and votes can be conducted on blockchain in a manner that is not at risk of being tampered with, misunderstood, or kept private. This way, everyone has access to election results, leaving no government or media solely responsible for reporting them.

This is already happening in South Korea with a platform called ICON.

Personal Identity

Rather than having a number, such as a social security number, your personal information could biometrically link to your DNA. Removing the possibility of someone stealing another’s identity or even assisting with the criminal justice system by eliminating wrongful conviction in cases with physical evidence.

Registering Information

Depending on physical papers to track your assets leaves significant room for error. Looking for your car title, electric bills, or birth certificate would no longer be necessary. Imagine if all your information existed digitally. You would not have to worry about keeping track of it.

This would also apply to businesses. The distributed ledger could securely store all articles of incorporation, taxes, employment records, pay stubs, office space, and all other business associated costs and documents. For example, instead of reporting your profits and losses each quarter, all of this would be available in real time.

Protection of Intellectual Property

Intangible ideas, designs, and work can get a trademark. But that doesn’t mean they’re safe from being forged or copied. It’s hard to prove an idea is uniquely yours. By registering intellectual property on the blockchain, anyone can trace it based on its timestamp. This can save time, money on lawyers, and a great deal of anguish.

File Storage

With the rise of the cloud, we saw data storage like never before. Instead of saving everything to a computer’s hard drive or external storage which could crash or be lost, there is now a location for storage which can be accessed anywhere with internet. However, cloud storage is a centralized application. Often the more storage you require, the more it costs. A cloud has a central point which an attacker can hack. By comparison, millions of computers worldwide host blockchain information.

Understanding Blockchain Information

We are human beings. We lose things, make mistakes and miscommunicate. There are countless other factors that can lead to issues and inconsistency. By comparison, when information is fully transparent and distributed, everyone is accountable for ensuring its validity and security.

The transparent nature of blockchain information allows individuals infinite avenues to uncover chronological, truthful information. As a result, the blockchain technology could radically shift the way we conduct countless transactions. Transparency allows us to form objective truths and hold each other and ourselves accountable.

What Is a Blockchain Wallet?

Before any transactions are made on the blockchain, an individual must set up a cryptocurrency wallet. One which is specific to the blockchain and widely utilized is blockchain wallet.

A blockchain wallet is an e-wallet which allows users to store two types of cryptocurrency: Bitcoin and Ethereum (ETH). It is entirely free to create a blockchain wallet and the process is done online. A blockchain wallet can be accessed on the blockchain website or on a mobile application. The only information you need to initialize and manage the account is an email address and a password. Once you’ve created your blockchain wallet you will receive a Wallet ID. A wallet ID is an equivalent to a bank account number.

Through the blockchain wallet interface, you can buy or sell cryptocurrencies. To make a purchase, you can transfer funds from a bank account, credit card, or debit card.

Once you are in, you will see your current balance for Bitcoin, ether, or both. You’ll also see your most recent transactions.

What Is a Wallet Address?

Each transaction has a unique address. An address is a series of letters and numbers which are a location to which you can send funds. In the case of bitcoin, a new address is created for every single transaction for security purposes. If you are looking to receive funds, you send a request with an address attached. If you are looking to send funds, the recipient provides you with their unique transaction request. Each transaction will incur a small fee. Transaction fees are in place to account for the mining fees and the blockchain infrastructure.

A blockchain wallet uses multi-level security measures to ensure that the contents of your blockchain wallet are safe at all times. The first level prevents users from losing access to their accounts through the creation of a 12-word backup phrase. The backup phrase can function in place of a forgotten password. The second security level prevents other individuals from accessing your blockchain wallet. You can do this by linking your phone number to your account. Finally, the third step gives users the ability to block Tor requests.

Getting to Know the Distributed Ledger

Blockchain can be challenging to grasp because it’s the technology underlying other, better-known applications. In other words, the distributed ledger is a platform you can use to democratize voting, streamline a supply chain, store data, create a currency and much more.

Unlike most technology, the collective, rather than an individual, controls it. This eliminates the need for third-parties in virtually all transactions.

Today, more industries than ever are transforming with blockchain. In other words, it’s only the beginning for the distributed ledger.